PSG portfolio manager HANNES SMUTS advises how you can avoid the risk involved with investing in shares.

Investing in listed equities makes you an owner of a share in companies listed on the Johannesburg Stock Exchange (JSE). It is exciting to be able to own part of Woolworths, Checkers, Vodacom, Mediclinic, Sasol, First National Bank, DStv and Capitec Bank, to name a few prominent household brands, all part of our daily lives. Equally, if not more exciting, is the possibility for local investors to invest via local stockbrokers in global companies such as Nestlé, Volkswagen, Coca-Cola, Apple, and Johnson & Johnson listed on international stock exchanges. Equities are a versatile investment class. The flip side of having so many options available is that equity markets have become something of a mine field. It can be increasingly difficult to make appropriate choices, especially for new investors. They find it best to employ the capable guidance of investment managers to assist in introducing and sticking to a few basic principles. If one gets it right, it can be a particularly rewarding journey.

Many successful investors and their advisers make no secret of the fact that they have achieved results, not by developing some magical formula, but merely by following the advice and proven strategies of seasoned investment gurus. Names that come to mind are Benjamin Graham, widely known as the ‘father of value investing’, and Warren Buffet, arguably the most successful investor of our time. Buffet’s passion for shares is best embodied in his well-known quote: ‘I made my first investment at age 11. I was wasting my life up until then’.

Closer to home, investors will do well to follow the advice of super-successful businessmen like the chairman of the PSG Group, Jannie Mouton, to whom Moneyweb refers as the ‘Boere Buffet’. Jannie attributes his knowledge to reading, reading and more reading. He stresses the importance of having time on your side, i.e. being patient and taking a long-term view when it comes to receiving rewards.

Paramount to this investment approach is the amazing power of compound growth; if you start with an initial monthly investment of R1 000 and increase it by 10% each year, an investment returning 15% per annum will accumulate to R57 million in 40 years. Jannie further shares a mistake to avoid – how he initially tried to make money through speculating in shares for short-term gains, and how he burnt his fingers. He says in 40 years he made no money through thoughtless speculation or ‘lekker tips’. So what is the appropriate approach to investment on the stock market?

To determine the suitability of any investment for your portfolio, you need to understand how returns are generated, particularly in the long-term. It is sensible to judge the suitability of a specific class of investment by comparing its likely return with that of other investment classes. For example, what the expected reward is for investing in shares, compared to property or a bank deposit. This boils down to assessing the risk associated with different asset classes (the higher the risk, the higher the likely return). Also, determine your risk appetite. Taking proper account of the different aspects of risk makes it possible for most investors to achieve a balanced investment portfolio containing a mix of different asset classes. Your investment objectives, which depend on your personal circumstances, should be realistic and in line with your ability to stomach risk. Low-risk, conservative investments tend to focus on earning income (interest, for example). Higher-risk investments seek to attain high growth of capital over time.

Typical examples of income-bearing investments are money market funds, government retail bonds and bank deposits. They carry a low risk of capital loss and aim to deliver the highest possible interest income. The downside is that investors have no growth on capital. On the other end of the scale are investments that are likely to show attractive capital growth over the long-term, but generate low or no income returns. These include art, antiques, vintage cars, rare coins, gold coins and other commodities. Certain shares also pay no, or very low, dividends. Most listed companies, however, do pay meaningful dividends, usually twice a year. Investments in this class are usually referred to as growth assets.

There is a perception among certain people that equity investments are only for gamblers and speculators. Perhaps it is due, in part, to the severe short-term volatility that equity markets exhibit at times. It is important to distinguish between punters of a certain share who chase a ‘quick buck’ and investors who weigh up risk, return and quality of company when selecting equity investments for a portfolio. The ‘easy money’ perception of investing in equities is often encouraged by the portrayal of equity trading in the media as being ‘easy’. Certain local and global institutions regularly advertise low-cost trading platforms, often combined with programmes promoting active, trading strategies, with these usually based on graphs, other technical aids and algorithms. Active share trading and its spoils have also been glamorised in movies like The Wolf of Wall Street.

How risky then is a serious investment in the stock market? Judging over long periods, its risk is no higher than, for instance, investment in property. Inherent risks are certainly there, but they can be managed by focusing on aspects you can control:

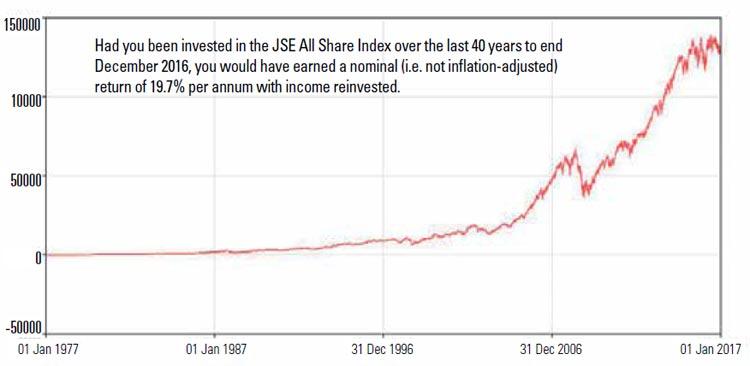

- The time period of investment. The most common mistake made by investors is to overreact to short-term price movements. Uncertainty often Owning your Piecoew n of theP ie advises how you can avoid the risk involved with investing in shares leads to short-term volatility in equity markets. During periods of negative news flow, share prices, even of top companies, could drop significantly. Certain investors are tempted to sell and move to the side-lines, believing that they will time re-entry into the market to their benefit. Research seems to indicate quite the contrary. For the 10 years to 11 August 2011, investors who remained fully invested in the JSE, would have earned 366%. If they missed the best 10 days their return would have dropped to 163%. If they missed the best 30 days their return would have been a paltry 15%. Jumping in and out of quality shares brings no joy.

- Risk diversification Equity investors reduce risk considerably by constructing a well-diversified portfolio, combining different asset classes, companies and sectors. Most will need professional guidance in this regard as over-diversification is likely to compromise returns as time goes by.

- The quality of the counters in your portfolio Select shares in companies with good management and a well-established business model. Most businesses are cyclical and will probably go through tough times at some stage. A quality company is one that will survive a slump and thrive again when its business environment improves. Investors must also assess an appropriate entry price in order to avoid paying too much for a share in a top-class company.

- The quality of investment advice Inexperienced or uncertain investors will do well to seek professional advice before embarking on their investment journey. Look for a suitably qualified adviser with ample experience. If he/she has the backing of an established investment house, it should add to your peace of mind.

Finally, successful investors have a specific mind-set. Jannie Mouton compares long-term investing to having a happy family - it requires lifelong love, care and dedication. As good friends carry you through emotional crises, quality investments carry you through economic storms.